12 best cashback credit cards in Singapore (2023)

PHOTO: Unsplash

Collecting air miles for your jet setting lifestyle admittedly sounds sexier than trying to scrounge for cash rebates. But if you're still one of those people who believe that cash is king, getting card benefits in cold, hard cash is just as appealing.

You literally get free money when you use a cashback card, and given that's there's no free lunch in Singapore, there's no way we're saying no to that.

So let's take a look at the best cashback credit cards in Singapore in 2023.

Here are our top picks for cashback cards with the highest cashback rates.

| Best for | Best cashback credit cards |

| Unlimited cashback | Citi Cash Back+, Standard Chartered Simply Cash, Amex True Cashback, UOB Absolute Cashback, CIMB World Mastercard |

| Regular expenses | UOB One, Citi Cash Back, HSBC Visa Platinum Credit Card |

| Online Shopping | DBS Live Fresh, OCBC FRANK, POSB Everyday |

| Low or no minimum spend | Citi SMRT, Citi Cash Back+, Standard Chartered Simply Cash, Amex True Cashback, UOB Absolute Cashback |

Move over, Citibank, because the new best cashback card on the market is UOB’s Absolute Cashback card. This card takes all the good things about Citi’s Cash Back+ card, such as the $0 minimum spend, and edges out the competition by adding a 0.1 percentage point to its rebates — at 1.7% unlimited cashback.

The only downside? It’s an Amex card, which means that it might be a challenge to find smaller merchants that accept it.

If you do stick to large merchants and put all your spending there, as well as bills, insurance premiums, school tuition fees, and the like, you’ll be able to get more mileage than the cards listed below.

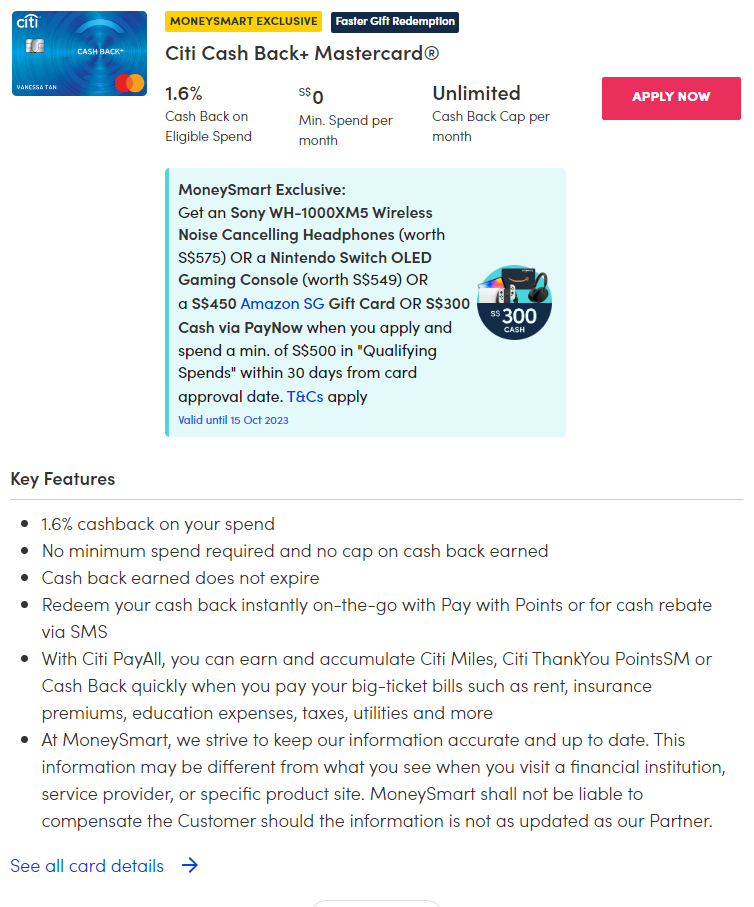

Unlike some cards which benefits look like they'll require a PhD to figure out, anyone with half a brain can successfully earn cashback on the Citi Cash Back+ Card.

Unlimited cashback cards like Citi Cash Back+ give you a flat cashback rate on everything with no cap. With no minimum spending or cashback cap, there's virtually nothing that would disqualify you from the 1.6 per cent cashback. This makes them ideal for big-ticket spending like wedding banquets or home renovations, which would bust the cashback cap on most other cards.

The Citi Cash Back+ Card currently plays second fiddle to UOB's Absolute Cashback card, offering 1.6 per cent cashback on all spending.

It does have one advantage-unlike the UOB Absolute Cashback card, which is an Amex card, the Citi Cash Back+ Card's card association is Mastercard. That opens up a wider range of merchants who'll accept it.

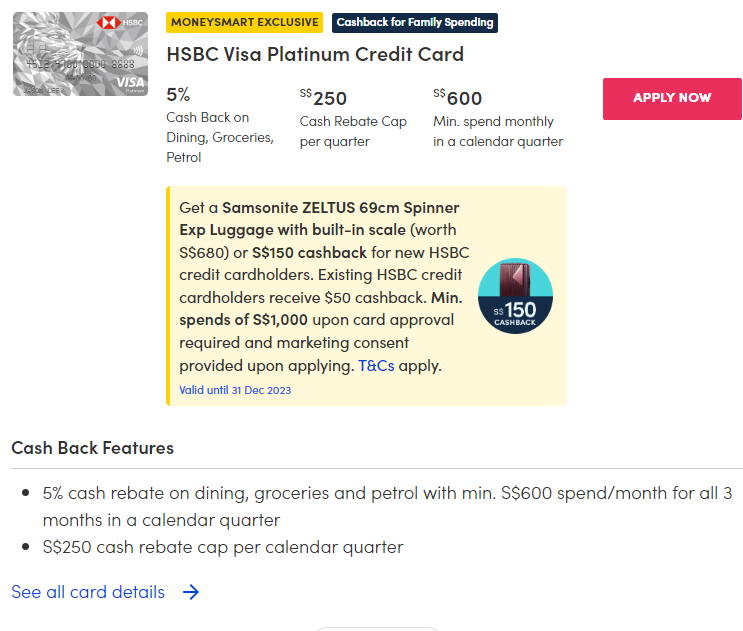

The HSBC Visa Platinum Credit Card is a great cashback card if you regularly spend at least $600 a month on dining, groceries, and petrol. That's because it offers up to 5 per cent cashback on those categories only if you hit this minimum amount.

On top of that, you'll receive complimentary access to Entertainer with HSBC-a food rewards app with 1-for-1 deals on dining, lifestyle, and travel worldwide.

There is a rebate cap of $250 per calendar quarter, which means that you will max out your cash rebates at a total spending of $5,000. Going to spend more than that in a quarter? Opt for an unlimited cashback card instead, such as the UOB Absolute Cashback Card, Citi Cash Back+ Mastercard or Standard Chartered Simply Cash Credit Card.

The Standard Chartered Simply Cash Credit Card is a nice-but-not-the-best-in-the-world cashback card. As far as unlimited cashback cards go, it's in third place after theUOB Absolute Cashback Card and Citi Cash Back+ Mastercard, giving you 1.5 per cent cashback on all eligible spending with no cashback cap and no minimum spending.

Here, "eligible spending" refers to pretty much everything barring the usual exceptions-bills, taxes, insurance premiums and any top-ups to prepaid cards or accounts.

Despite a slightly lower cashback rate than the Citi Cash Back+ Card, the Standard Chartered Simply Cash Credit Card has some advantages: for instance, its annual fee is waived for the first two years. It's also worth comparing their limited-time sign-up promotions to see which gets you a better welcome gift.

The Amex True Cashback Card is one of the longest-standing unlimited cashback cards around. It doles out 1.5 per cent cashback on all spending with no minimum spending requirement and no cashback cap. The card also offers 3 per cent cashback on up to $5,000 worth of spending in your first 6 months of use.

While the Amex True Cashback Card sounds like a better deal than the Standard Chartered Simply Cash Credit Card we just talked about, it's harder to get. The SC Simply Cash has a minimum income requirement of S$30,000 (Singaporean) or S$60,000 (Non-Singaporean), which is standard for an entry-level credit card. That's what the Amex True Cashback Card is NOT-its income requirements aren't even published, so it's up to Amex's discretion.

Do also note that the Amex True Cashback Card comes with an annual fee of $172.80. This is waived for the first year, but Amex is one provider that may not waive the card fee thereafter-no matter how nicely you ask.

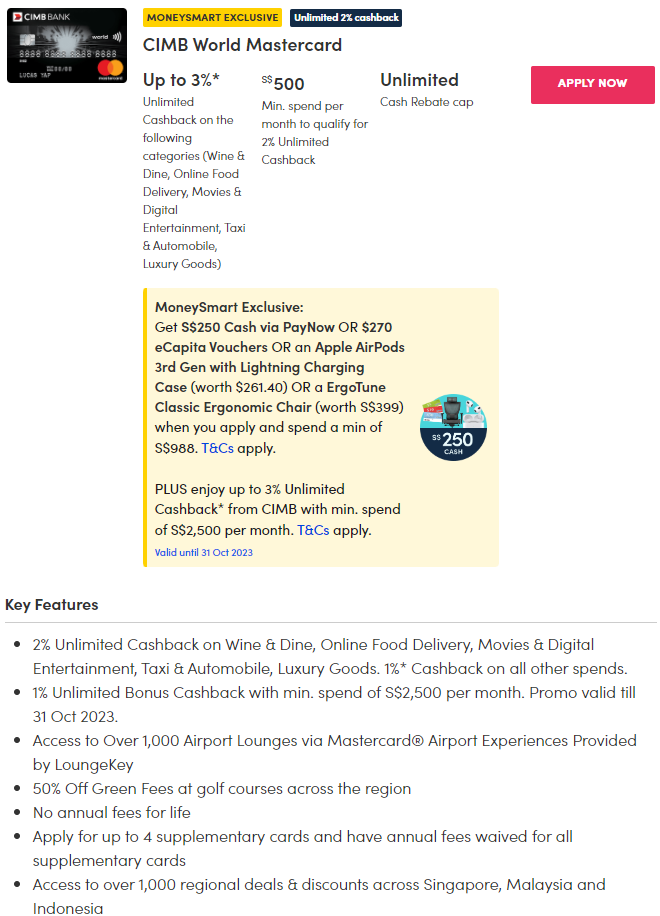

As far as unlimited cashback cards go, one that's often forgotten is the CIMB World Mastercard. No, despite it's name, it's not a miles card. The CIMB World Mastercard is actually quite a cashback heavyweight, bringing 2 per cent unlimited cashback to the table.

Wait, isn't that higher than the UOB Absolute Cashback Card and Citi Cash Back + Card? It is, but the catch is that this 2 per cent unlimited cashback applies only to selected categories, with a $500 minimum spend (this is a promotional rate valid till 31 Oct 2023). The selected categories are: Wine & Dine, Online Food Delivery, Movies & Digital Entertainment, Taxi & Automobile, and Luxury Goods.

On all other spends, you earn 1 per cent unlimited cashback. From now till 31 Oct 2023, you get an additional 1 per cent unlimited bonus cashback if you spend a minimum of $2,500 per month. That's no small sum, but it does make good use of your unlimited cashback.

If credit card fees-or rather, calling up the bank to get them waived-bother you, you'll be pleased to know that the CIMB World Mastercard promises no annual fees for life.

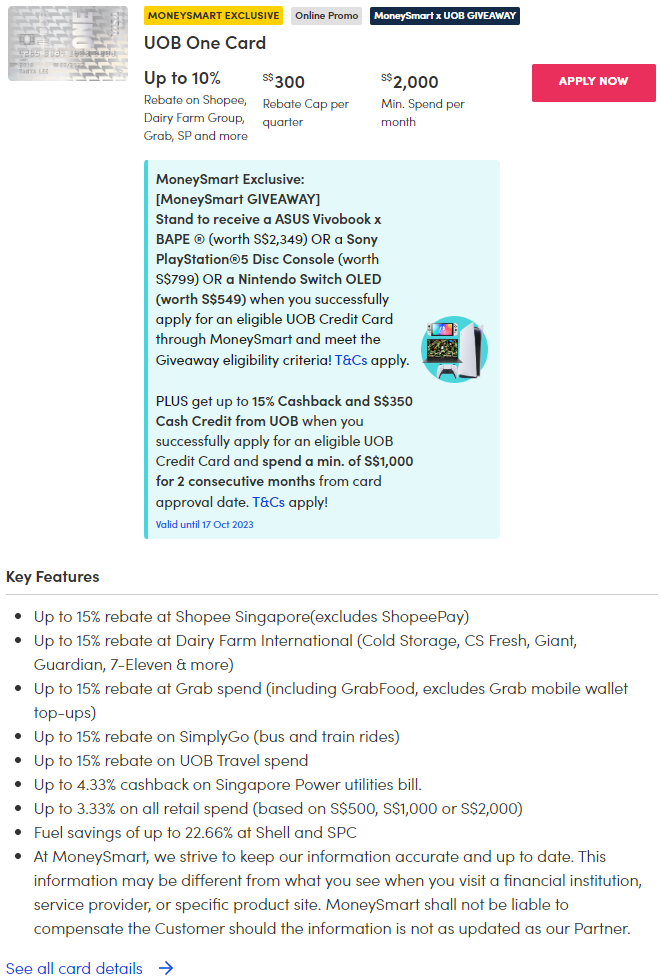

The UOB One Card offers some of the most generous cashback rates out there, but is reviled for its complex as hell mechanism. Suitable only for those who like a challenge.

| Cashback | $500/month and $1,000/month | $2,000/month |

| Base cashback per quarter | 3.33% | 3.33% |

| Additional cashback at selected partners | 5% | 6.67% |

| Enhanced cashback (for new card members who apply from now to 31 Dec 2023) | 6.67% | 5% |

| TOTAL | 15% | 15% |

The card gives you up to 3.33% on all retail spending if you spend $2,000 / $1,000 / $500 per month (at least five transactions) for three consecutive months. That’ll earn you a lump sum of $200/$100/$50 max cashback at the end of the quarter, which works out in all cases to up to 3.33% cashback.

However, in order to get additional cashback of 6.67% (making for a total of 10%) at partners like McDonald’s, Grab, Cold Storage, Shopee, 7-Eleven and SimplyGo, you need to hit a $2,000 monthly spend. If you only spend $500 or $1,000 a month, your bonus cashback is only 5%.

Finally, UOB is offering more bonus cashback they call the “Enhanced Cashback” for new UOB cardholders who sign up for the UOB One card from now till Dec 31, 2023. That’ll get you an additional 5% if you spend $2,000/month for three months, and 6.67% if you spend $500 or $1,000/month for three months.

If you add up the base retail spending cashback (3.33%), additional cashback at selected partners (5% or 6.67%), and UOB’s enhanced cashback (6.67% or 5%), you always get 15% whether you spend $500, $1,000, or $2,000 a month.

However, this is only because of their limited-time enhanced cashback, which gives $500/month and $1,000/month spenders more cashback than $2,000/month spenders.

At the current cashback rates, the UOB One card is indeed generous if you hit certain monthly spends. But once you hit the minimum spending requirements, it is a waste to spend more. So, you’ll need to monitor your spending on the card.

Not to be confused with the Citi Cash Back+ Card, the Citi Cash Back Card without-a-plus gives you eight per cent cashback on groceries and petrol and 6 per cent cashback on dining, provided you meet the minimum spending requirement of $800 in a month. Cashback on retail spending is a a meagre 0.25 per cent.

The total amount of cashback you can earn is capped at $80 each month, which means it's only worth spending $1,200 to $1,440 to earn maximum cashback.

DBS Live Fresh has rebranded itself as Singapore's first eco-friendly card made from 85.5 per cent recycled plastic, and offering up to 10 per cent cashback at certain eco-businesses.

Putting aside the greenwashing for the time being, the card's true benefit is actually 5 per cent cashback on online and Visa contactless spending, capped at $20 per month respectively. In other words, at the 5 per cent rate, the cashback maxes out at an expenditure of $400.

Now let's look at the eco-benefits of the card. The DBS Live Fresh Card also gives you an additional 5 per cent cashback at selected eco-friendly businesses, including:

Is there a catch? Yes, 2 in fact. Firstly, these cashback rates are subject to a minimum spending of $600 in a month.

Secondly, the cashback you can earn is capped. The cashback caps are:

This puts the maximum cashback you can earn in a month at $75-but you'd need to spend $7767 to get that. Realistically, you're only going to use the DBS Live Fresh card for the first three categories.

Don't be fooled by the OCBC Frank Credit Card's rather fluffy branding. It is actually one of the more solid online shopping credit cards out there, offering 8 per cent cashback on foreign spending and all types of local online/contactless mobile spending, whether for clothes shopping, grocery purchases or your Netflix subscription.

Like the DBS Live Fresh Card, the OCBC FRANK Credit Card is also offering higher cashback if you go green. You can enjoy an additional two per cent cashback when you shop at selected eco-friendly merchants, such as Scoop Wholefoods, Little Farms, SimplyGo, and BlueSG.

The minimum spending requirement is $800 in a month, with a monthly cap of $1oo cashback. To further break down the $100 cap, it's actually a $25 cap per category among these four spend categories:

The Citi SMRT Card has all the glamour of an Ezlink card, but who cares when it's giving you a generous five per cent cash back on groceries, public transportation and online shopping. That is, if you meet the minimum spend of $500 a month-otherwise, it's a paltry 0.3 per cent base interest rate.

Do note that when they say cashback on online shopping, they're excluding travel-related transactions.

Total cashback is capped at $600 every 12 months, which works out to $12,000 worth of spending per year.

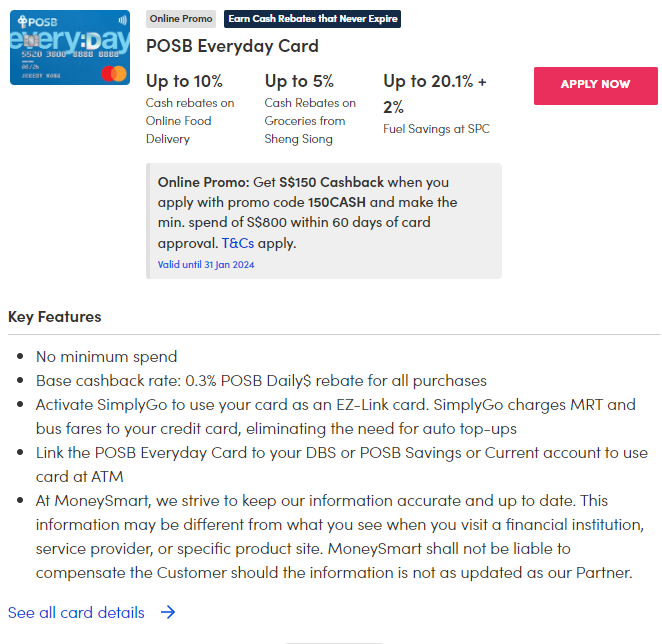

The POSB Everyday Card doesn't look very alluring, but it's good enough for life's basic needs. There is no minimum spending requirement for you to earn 5 per cent cashback at Sheng Siong. For pet owners, use this card at Pet Lovers Centre for three per cent cashback on regular-priced items, provided you hit the $15 minimum purchase amount.

If you drive, it also gets you 20.1 per cent savings at SPC-everyone's favourite cheap petrol kiosk.

On top of that, if you do spend at least $800 a month, you can unlock rebates of 10 per cent on foodpanda and Deliveroo delivery, eight per cent on selected online shopping merchants such as Amazon.sg, Lazada, Shopee, RedMart, and iHerb, as well as three per cent at Watsons and on dining expenses.

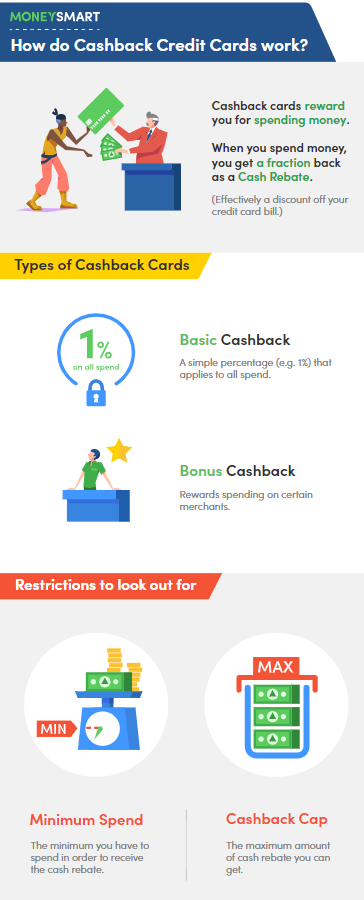

Before you get too excited about that hefty bonus cash rebate, remember that banks aren't charities. They have to impose minimum spend requirements and cashback caps, or else they'll just bleed money. So don't get led astray by big fat cashback promises-the important details are usually in the T&Cs.

Here's how they work:

ALSO READ: Best credit cards for lazy people (2023): Low maintenance, hassle-free payments

This article was first published in MoneySmart.